In today’s economic climate, millions of people across North America are forced to make difficult financial choices. From sudden medical bills to unexpected job loss, moments of uncertainty often push people toward high-interest, short-term solutions. But while these options may promise relief, they often create deeper long-term struggles that prevent lasting financial growth.

The Pressure to Act Fast

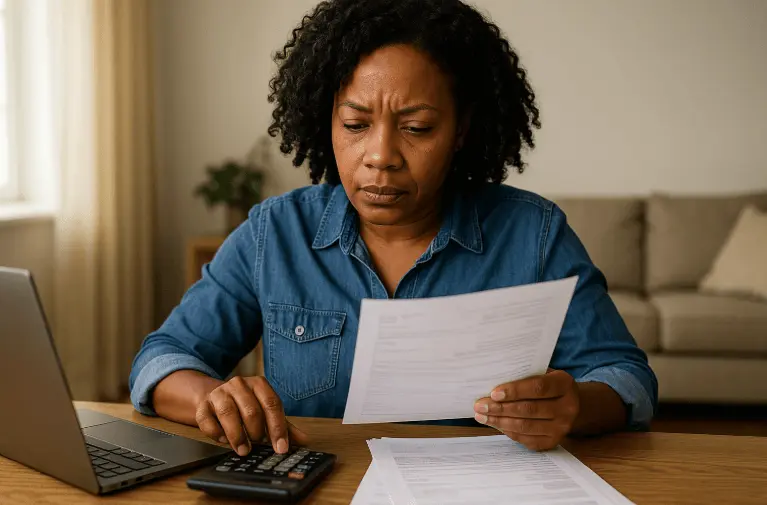

When you’re living paycheck to paycheck, financial emergencies rarely wait. A broken-down car, a missed rent payment, or a surprise school expense can become a crisis overnight. The pressure to find immediate cash can lead many to take out payday loans—fast-cash advances that seem convenient at first glance.

But what happens after that initial sense of relief? Often, these loans come with sky-high fees, short repayment periods, and the risk of getting trapped in a cycle of borrowing. The result? A deeper financial hole, increased stress, and a long road to stability.

A Look Beyond the Quick Fix

Instead of relying on short-term fixes, many financial educators and wellness advocates recommend taking a step back. Emergencies reveal where our systems need strengthening—not just our budgets, but our strategies, too.

For those willing to consider long-term stability over instant solutions, there’s good news: there are borrowing alternatives that offer real support without the long-term risk. Installment loans, for instance, provide predictable repayment plans, lower interest rates, and are often more flexible than payday loans.

EasyFinancial, a Canadian lender, offers installment loans that have been positioned as a safer and more reliable loan option for individuals seeking short-term relief but long-term progress. These options are especially helpful for those looking to manage one-time expenses without risking repeated borrowing or high penalties.

The important takeaway? Empowerment begins not just with access to credit—but with access to the right kind of credit.

Education as a Financial Tool

Many communities—particularly those historically marginalized—are not just dealing with cash flow problems. They’re dealing with the emotional and educational burdens of generational financial disadvantage. That’s why it’s critical to pair financial tools with financial knowledge.

Learning how credit works, what interest rates mean, and how repayment schedules can impact your long-term financial profile empowers people to make smarter decisions. And that knowledge often starts at the community level—through trusted voices, peer-led education, and platforms like JiceJohnson.com that promote financial confidence alongside cultural awareness.

A payday loan may seem like the only solution in a moment of need, but education shows us otherwise. It opens the door to more thoughtful alternatives and gives people the power to choose the right solution, not just the fastest one.

Breaking the Borrow-Spend Cycle

Many of us weren’t taught to think about money as a long game. Financial advice in many households boiled down to “pay your bills” and “don’t owe anyone.” But in today’s world—where credit scores determine access to everything from apartments to business capital—understanding how to build and use credit is essential.

The borrow-spend-borrow-again cycle is the trap many payday loan users fall into. Instead of escaping the debt spiral, they get stuck, sometimes paying back double or triple the original loan amount just to stay afloat.

By contrast, longer-term installment loans can offer more forgiving repayment schedules and the chance to build credit at the same time. This isn’t just a financial benefit—it’s a psychological one. People start to feel in control of their finances again. They begin to rebuild confidence.

And with confidence comes possibility—whether that’s starting a business, going back to school, or simply saving for the future.

Building a New Normal

Access to fast cash will always have its place, especially in urgent situations. But as communities begin to focus on generational wealth and financial literacy, the conversation has to evolve. What tools are we handing to the next generation? What habits are we modeling?

Choosing a safer and more reliable loan option over a quick fix is more than a financial decision—it’s a cultural shift. It says: “I’m not just surviving. I’m building.” And that’s a powerful message, especially in communities where economic independence hasn’t always been within reach.

Jice Johnson’s mission—promoting legacy-building and empowerment through knowledge—is deeply aligned with these values. Whether it’s through education, entrepreneurship, or smarter financial decisions, the goal remains the same: freedom through informed choices.

Final Thoughts: Your Future, Your Terms

There’s no shame in needing help. But there is power in knowing your options. The more we educate ourselves and each other, the better equipped we are to choose pathways that support long-term success—not short-term relief that leads to regret.

Financial independence isn’t just about having money in the bank. It’s about understanding how the system works, how to use it to your advantage, and how to protect your peace in the process. When the next emergency comes—and it always does—you deserve more than a high-interest loan.

You deserve tools that build you up, not wear you down.